Mon 23 Dec 2024 - Paul Scott's Small/Mid Cap Value Report

Free: DLG, BOO, PFC, RBGP, QUIZ Premium: SEE, PRM

MrC's Smallcap Sweep: Culling time at the Last Chance Saloon

BOO, HAYD, DLG, PFC, SEE, ITM, GOOD, NAH, KRM

◄boohoo (BOO)► like an unravelling jumper, snagged on the thorn of hubris, BOO continues its backwards journey as it completes the agreed sale of its flagship SOHO HQ for £49.5m. It paid £72m. [SP=33.14 Cap=463m]

◄Haydale Graphene Industries (HAYD)► outcome of business review: resources are currently spread too thinly. Co to "focus on highest potential product and service offerings include those for enabling carbon reduction". Will get shot of its US business. Will "streamlining operations to enhance efficiency and significantly reduce costs". Major holder Simon Turek to become CEO. [SP=0.12 Cap=5m]

◄Direct Line (DLG)► agrees 275p offer from Avaia: c.130p cash + paper. [SP=242 Cap=3174m]

◄Petrofac (PFC)► d4e rescue recapitalisation with "material dilution, while preserving some value, for existing shareholders". [SP=10.21 Cap=54m]

◄Seeing Machines (SEE)► c.£26.2m 'strategic' subscription at 4.09p, a 17% discount, by Mitsubishi Electric Mobility. Boosted as a "unique opportunity to seize growth with world class partner". [SP=4.45 Cap=191m]

◄ITM Power (ITM)► sells three NEPTUNE V units for delivery in H1 2026. No £££. [SP=34.72 Cap=214m]

◄Good Energy (GOOD)► PUSU deadline extended. [SP=371.5 Cap=69m]

◄NAHL (NAH)► discussions with final bidders for Bush & Co. are progressing. I hold. [SP=66 Cap=32m]

◄KRM22 (KRM)► delays interest repayment date on £5.m convertible loan. The interest rate and covenants are unchanged. [SP=30 Cap=10m]

Good morning from Paul! EDIT - sorry it’s tomorrow that the market is a half day. Today is a full day!

Meet my new co-writer David Wilde - who introduces himself here -

“After obtaining my degree and masters (focussed on finance, accountancy and operational research) from the University of Edinburgh, I worked in the IT and strategy departments of a FTSE 100 company. After deciding this wasn't the life for me, I started a small software company that allowed me to travel and pursue outside interests, including music and water sports.

After winding down the company to focus on my family, I've returned to studying investing and have been managing my own SIPP for around a decade. My approach is constantly evolving as I continue to learn (particularly from mistakes!) but currently it's probably best described as being in the GARP camp. I enjoy evaluating companies where a deep, forensic evaluation can uncover something unknown to the wider community and where effort can provide an edge. However, I recognise that it often takes me down useless rabbit holes and that the time would be more productively (but less enjoyably!) spent elsewhere.

I'm thrilled to be working with Paul and to join the incredible investors in his community on a communal learning experience that is both rewarding and enjoyable for us all!”

A warm welcome to new premium subscribers over the weekend - Mike, Joe, Anthony, Mike, Derek, Rob, Mark, and Simon.

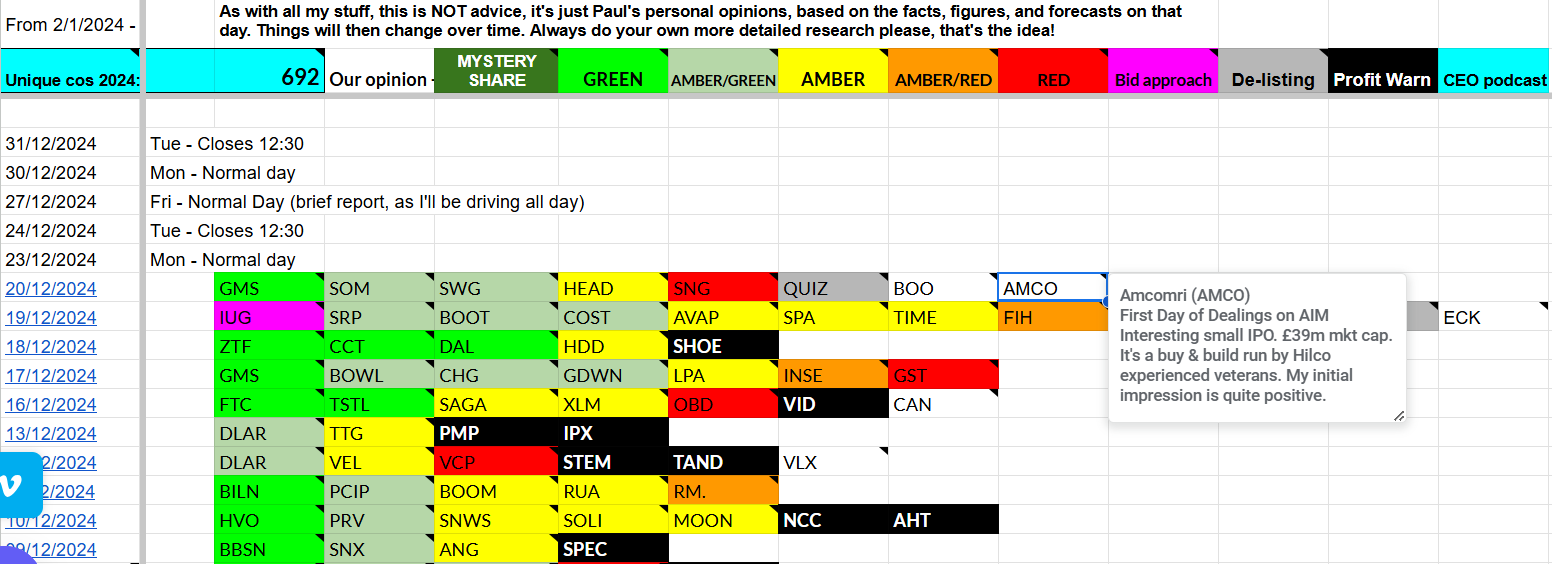

Link to my spreadsheets, for premium subscribers only (please don’t share these links). This is now fully up-to-date for calendar 2024 - here’s a reminder of the format - hovering over any cell causes a pop-up to appear with a short summary from me (search by ticker using CTRL+F) -

Top 20 (or maybe 25) share ideas for 2025 is nearly finished now, and I’ll be publishing that on or around 31/12/2024 - to paying subscribers only. So if you want to see that, now is the time to join the happy throng here!

Will I be able to repeat the barn-storming performances of 2023 and 2024 in 2025? Probably not, we have to set expectations at a realistic level. In both years my share ideas list beat the AIM index by just over 30% - admittedly not the most challenging of benchmarks, but I use it because half or more of my ideas were AIM-listed.

Podcasts - I’m trialling a new idea today, with 2 podcasts going out simultaneously - a shorter free one, and a more comprehensive, longer one for premium subscribers.

Direct Line (DLG)

Up 3% to 250p (£3.28bn) - Recommended cash & share offer for DLG - PINK

Terms unchanged at 129.7p cash + up to 5p divi, and 0.2867 new Aviva shares. Total value is 275p (actually 266p at Aviva’s live price today) - that’s the same as the indicated terms announced in early Dec, so today only confirms the deal and moves it along to a formal offer. It’s a decent 73% premium to the undisturbed price, but well short of previous highs of 300-350p that it mostly hovered around from 2016-22.

Boohoo (BOO)

Unch. 33p (£463m) - Sale of London office - Paul - AMBER (at best)

Has sold London office for £49.5m (Paul - a loss, but property prices have fallen). Will repay remainder of term loan in full, and says £125m RCF remaining is sufficient for its future needs (Paul - not if it keeps generating trading losses). I’m not at all convinced that the sum-of-parts exceeds current market cap, which is what they’re telling us. Shein has clobbered the fast fashion sector, so the only hope is if Govt action blocks Shein from direct imports into UK. Why would they do that when trying to attract Shein’s IPO to London?

Petrofac (PFC)

Down 22% to 8.0p (volatile) £42m - Comprehensive Financial Refinancing - Paul - RED

I flagged this one as RED several times earlier this year, starting in April, as it’s an obviously financially distressed situation - which I’m sure everyone already knew, but bulls gamble on a potential multibagger in this type of situation, if they can avoid big dilution.

There are several key elements to this refinancing -

Debt to equity conversion of $772m, eliminating the bulk of its debt.

New debt of $131m.

New equity of $194m.

Retail offer is only $8m!

Extinguishing some historical actual & contingent liabilities re Thai Oil contract.

Restructuring expected to complete in Q1 2025.

Bank lenders have not yet signed the deal (but bondholders have).

As you can see below, existing equity is almost wiped out, with only a trivial 2.5% post deal -

There are also some nil-cost 5 year warrants triggered by the future market cap reaching $1.3bn and $1.95bn thresholds.

It’s very complicated, this announcement, and hopefully I’ve not missed, or misinterpreted anything important. I’ve tried to find out the terms of the new equity issuance. This seems to be it -

“The New Equity capital raise is being conducted by way of a non-pre-emptive placing and, together with the issuance of ordinary shares in the debt restructuring, it will result in material dilution for existing Shareholders. In aggregate, 20,550m ordinary shares will be issued, representing 97.5% of the Company.”

There seem to be c.522m shares in issue currently. So at a current share price of 8.0p, that would make the market cap £1.68bn once the share count has become just over 21bn shares post refinancing. That looks too high given dismal operating profits (losses since 2021) recently, although pre-pandemic Petrofac was making c.$500m pa operating profit.

Post refinancing PFC would have a much improved balance sheet, and debt at only modest levels.

Paul’s opinion - the current share price still looks considerably overvalued. Sub-5p looks a lot more realistic, given the huge number of new shares that are being issued. Even then, you need to be an enormous optimist to imagine PFC can be turned around, let alone return to previous levels of profits.

I can’t see why anyone would get involved in this can of worms.

However, today’s news suggests that existing holders will salvage something from the wreckage, but was it worth the risk?

I’m sticking at RED, because a £1.68bn market cap post-fundraise still looks much too high.

It’s very impressive that management have managed to save anything for existing equity, and avert insolvency (assuming the banks agree, and the deal goes ahead, it might not). Definitely not a falling knife to catch, in my opinion.

RBG Holdings (RBGP)

Unch. 2.9p (£4m) - EGM Requisition - Paul - RED

I last reviewed the fundamentals on Stockopedia here on 4/10/2024, concluding that things were so bad, the existing equity looked worthless. The balance sheet is very weak, in particular with insurmountable bank debt. The attempted trading turnaround has not worked. Press reports had previously suggested that Ian Rosenblatt, 20.5% shareholder and closely involved with the Rosenblatt’s branded solicitors owned by RBGP, was trying to turf out management (who seem pretty useless, so I don’t blame him).

Today’s news is that RBGP announces it received (on Friday) a requisition for an EGM from Ian Rosenblatt, to remove the CEO and two NEDs. Horses, and stable doors spring to mind. As is customary, shareholders are “advised to take no action at this time”. What action can they take, other than selling in the open market, if possible?

Paul’s view - I’ve dropped a few hints already above, but this is like a mini-Petrofac, in that it’s blindingly obvious an equity fundraising is overdue. The problem is, we have no way of knowing on what terms that’s likely to be, if at all. We saw with Petrofac how bad these can be, with existing equity to be diluted from 100% to 2.5% ownership of the company. Something similar might happen at RBGP, who knows?

A more positive view is that Ian Rosenblatt might want to preserve the value of his existing holding, and put in fresh money at a more favourable price. Why would he though? Who knows, I’ve not met him or discussed it. Surely the most obvious solution would be for Mr Rosenblatt to do a deal with the bank to buy out the operating subsidiary and then let the plc holding company go bust? I think there are added complications if solicitors go bust, in terms of possibly losing accreditations, etc, but I don’t know any details.

I cannot understand why anyone would want to gamble on the existing equity, when the business is so obviously in severe financial distress, as a refinancing could so easily wipe out existing holders. Anything could happen, but it’s difficult to see much upside for equity until a refinancing has been done. So risk:reward strikes me as absolutely terrible here. RED again.

Quiz (QUIZ)

Down 60% to 0.9p (£1m) - Delisting - Paul - GREY (delisting)

I covered this in Friday’s report, when it announced late that it intends to delist.

Not a surprise, the delisting risk has been obvious since June, or earlier even. Another one bites the dust - a good thing for the market overall I think - we need a big clear-out of failed companies from AIM, and then hopefully it can be refreshed with some decent new floats (ever the optimist!)

Free content ends here.

Keep reading with a 7-day free trial

Subscribe to Small/Mid Caps with Paul Scott to keep reading this post and get 7 days of free access to the full post archives.