Thu 7/11/2024 - Paul Scott's Small Cap Value Report - HWDN, CABP, WG., KITW, SBRY, FDEV, SFOR, ITV

This article is now complete.

Good morning from Paul!

NB. I’ve restructured my Substack, so it’s now more like a website, hopefully you find it much better (and improved comments). So please bookmark this new link in your web browser, which is my home page.

Today’s article is now finished. I’ll just record today’s podcast, then it’s time to slope off to the Mary Shelley for a late lunch and a pint! Here it is -

Bank of England cuts base rate by 0.25% to 4.75%, as expected.

Day 3 of my new venture! Thanks for all your support, and lovely messages (it was like reading my own obituary on Stockopedia!). I’m delighted with the number of followers/reads/thumbs ups, and most importantly a good number of you have also pledged to subscribe when I turn on subscriptions in about 2 weeks - hugely appreciated, thank you!

My plan is to employ a team of writers in the longer term, but obviously I need to get subscription revenue up to a higher level first where that becomes affordable. There’s a long way to go, but we’ve made a terrific start, thank you!

What is the Founder Member option? It seems to be an optional, higher annual subscription, for people who want to show their support the most. It’s not my idea, it’s just a Substack feature. Maybe it gives bragging rights of some kind, I’m not sure!

I adjusted a lot of settings last night, as I gradually find my way around Substack. Comments should now be ordered as newest at the top. If you bookmark substack.com/@paulypilot in your web browser, that is basically my home page here - just treat it like a website. The Substack phone app is very good too, and quite easy to use. We’ll get the hang of it, early days still!

Disclaimer - all my stuff is purely opinions, never advice. It is vital that you do your own, more detailed research please, and take professional advice if required. I don’t know what the future holds, so some of my share ideas will work, and others won’t - and I change my mind as the facts change.

Summaries of main sections below -

John Wood Group (WG.) - down 41% to 73.5p (volatile) £509m - Q3 Trading Update - RED

A confusing Q3 update that sounds a little soft, but FY 12/2024 guidance is reiterated. So why the 41% plunge in share price? I think it’s down to a reduced order book, lack of 2025 guidance, but above all news of a wide-ranging accounting/governance review required by the auditors. Add that to its already awful balance sheet, with too much debt, and asbestos liabilities, and I think this is uninvestable for now. So am dropping from amber/red last time, to RED.

Kitwave (KITW) - down 1% to 335p (£269m) - Trading Update - AMBER/GREEN

Another in line update, saying that FY 10/2024 ended as expected. It’s quite a nice business, and has scaled up a lot with a big acquisition in Sept. Debt is quite high, but not alarmingly so. I think the valuation is fair, possibly with a bit of upside, so I’m happy to stick at moderately positive amber/green.

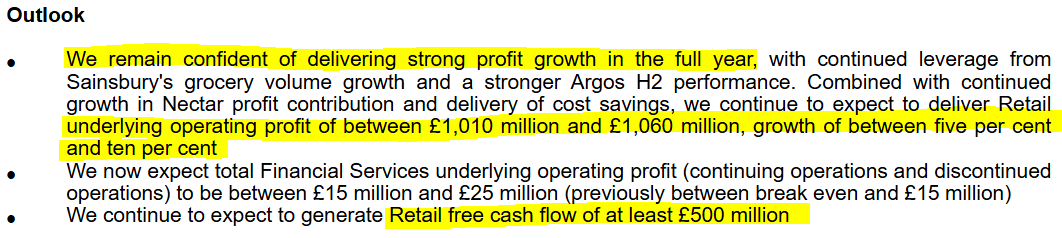

J Sainsbury (SBRY) - down 1% to 264p (£6.25bn) - Interim Results - AMBER

Bullish sounding commentary with its H1 results drew me in. This is actually quite good, overall I’m impressed. It’s trading reasonably well, Shore slightly raises full year forecast, and there are impressive divis & balance sheet with lots of freeholds. Horrible sector though. Supermarkets seem to have been able to cope with big increases in wages costs in recent years, by raising prices. Note 16 flags the potentially substantial cost of a recent equal pay tribunal ruling - no provision has been made in the accounts yet.

Brief comments

(news & big % movers) -

Mobico (MCG)

Up 7% to 76.6p - Q3 TU - AMBER

The market likes this update from this transport group, mainly buses. FY 12/2024 profit will be in line with expectations (185-205m range at operating profit level). Good revenue growth of +12% in Q3, from good passenger demand growth. Cost savings on track. Divestment of N.American school bus division is also “on track” - estimated sales proceeds from brokers are a very wide range, so clarity on the likely proceeds is needed.

Paul’s opinion - I like the turnaround/disposal story here, but was spooked by an FT article which highlighted c.£500m hidden debt - which is cleverly structured to appear to be like equity, but it’s clearly actually debt. That radically changes risk:reward I think, and put me off. I wrote an article about this on Stockopedia on 23/8/2024. Hence I can’t get above AMBER for now.

ITV (ITV)

Down 8% to 66.4p - Q3 TU - NO COLOUR

I was positive on this TV company at 76p on 9/5/2024, when it announced the pension scheme was fully funded. It peaked in July, but has come off about 20% since then, including today’s fall triggered by revenues falling. Surprisingly, it mentions continuing impact from the 2023 US writers & actors strike. More cost savings announced. I’m too tired to do a full review of this now today, and ITV trading updates are always dreadfully confusing - who writes this crap?! There’s way too much detail, but no clear overview. But with a >7% dividend yield, plus buybacks, and a reasonable balance sheet, this share could be worth you doing some proper research on (let me know what you think).

S4 Capital (SFOR)

Down 8% to 36p (£223m) - Q3 TU - AMBER/RED

A mild profit warning. Dowgate says Q3 was “marginally below” its forecasts. Net debt guidance is retained, and is well within covenants, with long maturities, so I think SFR has time to turn itself around hopefully.

Overall though, my view remains that SFOR is a pile of crap with a horrible balance sheet, but the lower the shares go, the higher the chance for sharp rebounds on any good news, perhaps? Although previous bounces have fizzled out. If Dowgate’s forecasts work out (£44m adj PBT FY 12/24, recovering to £62m in 12/25), then this share could surprise on the upside. Hence I wouldn’t bet against it, even though I still think it’s poor. Other concerns are the outrageous golden share arrangements for Sir Martin (giving him personal control), and the excessive adjustments to the accounts, obscuring the real performance.

Frontier Developments (FDEV)

Down 17% to 248p (£97m) - New game flopped?

No company news today, but searching online there is talk of a new game launch Planet Coaster 2 possibly flopping, with bad reviews. Hopefully we’ll get more information if this story develops.

CAB Payments (CABP)

107p (pre-market) £271m - Bid talks off - AMBER/RED

I suspect this payments company might take a tumble today, as StoneX announces it does not intend to make a bid. (EDIT: down 22% to 83p in early trades)

Previously on 11/10/2024 we were told that NASDAQ listed StoneX was considering a 145p offer for CABP.

On 20/10/2024 it was confirmed that discussions and due diligence were underway, but also a profit warning saying that H2 trading was slower than expected at CABP.

Today it talks up strategy & strategic progress, and expected “sustainable growth from 2025 onwards”, reinforcing to me that trading in 2024 is not very good!

Paul’s view - I’m nervous about CABP, it seems accident-prone, and I’m not keen on the payments sector anyway. This was an over-priced main market float in July 2023, which disappointed quite quickly, losing two thirds of its value by Oct 2023 on a profit warning. Just safest to steer clear altogether I think.

(note from flags on the chart at Stockopedia, we covered it 3 times around the time of the late 2023 share price collapse)

Howden Joinery (HWDN) £4.67bn

TU - AMBER

(EDIT: down 4% to 811p in early trades)

LfL revenue growth turned negative -1.9% in H2 so far, vs +2.6% in H1. Self-help measures taken on cost & efficiency. Market share gains.

Expects FY 12/2024 profit to be at lower end of range of analyst forecasts (no footnote). Outlook for 2025 “to remain challenging”. Budget impact - “still assessing” overall financial impact., but c.£18m higher cost from employers NICs (5.5% of 2023 PBT).

Paul’s view - forecasts likely to come down, I suspect (no access to broker notes yet). Nice business, with excellent long-term track record, but valuation looks full, at fwd PER 16.2x, given that the estimates are likely to fall. Yield is low at 2.7%, so I don’t see much short-term attraction to this share.

Major multibagger from the 2008/9 lows, but it’s a mature business now, so growth is a lot slower now in percentage terms.

Main sections

J Sainsbury (SBRY)

Down 1% to 264p (£6.25bn) - Interim Results - AMBER

I’m curious to see what this supermarket + Argos group says about increased wages costs next year (but didn’t find anything - please leave a comment if you found any info on this).

The commentary today sounds very bullish about market share gains, but the H1 underlying numbers don’t particularly impress -

H1 revenue +3.1% to £16.3bn

H1 underlying PBT +4.7% to £356m - tiny profit margin, as it’s such a competitive sector.

Non-lease net debt is pleasingly low at just £152m.

Banking operations are being sold, which should make the results & balance sheet simpler to analyse.

Balance sheet - is large, and complicated. However NAV looks healthy to me at £6.6bn, including £811m intangible assets, so a comfortable £5.8bn NTAV - very similar to the market cap, so investors are almost completely asset-backed here. Note the pension schemes are huge, over £5bn in both assets and liabilities, but showing an accounting surplus of £776m. In actuarial terms, it still has to pay in - £45m payable for FY 2/2025. That could change when the next 9/2024 triennial actuarial numbers are calculated. There are big numbers for assets/liabilities pending disposal, just so you’re aware.

Checking its last annual report, note 14 shows that SBRY owns a remarkable £7.8bn in “land and buildings” - which I think is all freeholds, in the books at cost. That number excludes the leased property right of use assets, and fixtures & fittings. So this looks a property-rich group - could that attract a bidder when the next property boom cycle starts? Google tells me it owns the freeholds of about 60% of its stores - if that’s true, it’s a big plus for this share.

Outlook - positive in tone, although not sure I would agree that 5-10% profit growth is “strong”. It’s OK rather than strong I’d say -

Broker update - thanks to Shore Capital, which slightly raises FY 2/2025 forecast profit by just over 1%, and EPS is forecast at 22.0p - so a PER of 12.0x - that sounds about right to me.

The main attraction here is a decent yield, as it pays out c.60% of earnings in divis - forecast at 13.5p for FY 2/2025, yielding 5.1%.

See note 16 on contingent liabilities. This has put me off. It’s facing 11,900 equal pay claimants, with more expected, due to a controversial recent employment tribunal finding. I think until this issue is settled, one way or another, it rules out the share for me. There has not been any financial provision booked as yet, due to uncertainty.

Paul’s view - only a quick review, as I haven’t checked out Sainsburys for a long time. As a customer, I’ve noticed they seem to be delivering much better value and offers, and although only based on one store, it strikes me as well managed. An incredibly difficult, competitive sector, and of course the onward march of Aldi and Lidl is a threat. Although so far, SBRY seems to be successfully holding its own. I like the balance sheet with lots of property, and the divis aren’t bad.

Let’s go with AMBER - I would be higher, but the risk from the employment tribunal issue puts me off for now.

Kitwave (KITW)

Down 1% to 335p (£269m) - Trading Update - AMBER/GREEN

Kitwave is a buy & build group, distributing goods (typically food & drink) to lots of customers. Acquisitions are often to add new geographical areas within the UK.

I last looked at it on 3/9/2024, after a reassuring summer (peak period) trading update confirmed it should meet FY 10/2024 profit expectations. I was AMBER/GREEN, concluding that it’s a nice enough business, but growth is a bit sluggish, and it’s taken on more debt to fund acquisitions.

September saw news of a much bigger acquisition, Creed Catering Supplies, for £60m (plus up to £10m 2-year earn out), funded partly with a £31m equity fundraise at 305p. The balance was funded from a £29m increase in bank debt. On 24/9/2024 it said (re bank debt) -

“The enlarged Group is expected to have average leverage below 2.5x on a pro forma basis in the financial year ending 31 October 2025, falling to less than 2.0x as at 31 October 2025 (under 1.5x leverage on an ex IFRS16 basis).”

Roll forward to today, it again confirms trading is as expected and FY 10/2024 was in line with market expectations.

The key issue of rising employers NICs is mentioned -

“The Group has reviewed the implications of the recent budget announcement by the UK Government. As part of its forecasting, the Board anticipated some of the changes that were announced such as the increase in the national minimum wage. The reduction in the national insurance threshold was not anticipated, and when combined with the rise in the employers' national insurance rate to 15% the effect is to add c.£2 million to the Group's annual operating costs. Given the changes will only take effect from April 2025, the Board plans to mitigate this additional cost through efficiencies and other savings in the current financial year.”

That’s a really important point actually. I’ve been panicking a bit over this point, expecting profit warnings, but KITW makes the excellent point that they’ve got time (until April 2025) to take actions to mitigate, where possible. Same for all companies. So actually, we probably won’t see a flurry of immediate profit warnings as I feared, but I still think we’re likely to see lots of brokers reduce 2025 forecasts due to the triple whammy of higher ERs NIC, the lower threshold (costing £615 pa for all employees earning over £9,100), and another big hike to minimum wage. Lots of companies will be raising their selling prices in April 2025, that’s for sure - if not before, to test what their customers will tolerate. Overall inflation is also likely to rise in the spring of 2025, thus possibly stopping further interest rate cuts by the Bank of England?

Greater scale - the acquisition/placing announcement on 24/9/2024 gave an indication of the pro forma scale of the enlarged group - and I can see why this matters, as it should bring more buying power from greater scale - a key point for any distributor -

“a significant increase in the financial scale, with the enlarged Group expected to achieve pro forma3 revenue of over £800 million, adjusted EBITDA of £55 million and adjusted operating profit of £42 million”

Paul’s opinion - I think my previous AMBER/GREEN view stacks up still, as nothing has really changed.

The PER on FY 10/2025 forecasts is only 10.3x, but you have to remember there’s substantial debt here now. Plus a distribution business won’t command a premium PER. There’s also some risk with big acquisitions, as companies don’t always end up with what they thought they were buying. Although when it’s in the same sector, they probably already know the target company pretty well.

Canaccord reckons it should end FY 10/2024 with £62m net debt, falling a bit to £57m the year after. That limits divis a bit, and note the yield is about 3.6%.

Overall, I think it looks moderately positive. There could be some upside on the share price over time, maybe. Businesses like this are all about management being fanatical about controlling all the details, and operational excellence. So talking to customers and employees would probably be the best research you could do - is it run like a tight ship, or a shambles? I recall hearing (too late unfortunately) that when Conviviality went bust (blowing a £30k hole in my pension) it was apparently common knowledge that they were in a total shambles, with deliveries & invoices frequently being wrong. Hence I would now never invest in any distribution business without being sure that the machine was well-oiled and working as close as you can get to flawlessly.

The chart below is a great rarity - a 2021 AIM float that has risen!

John Wood Group (WG.)

Down 41% to 73.5p (volatile) £509m - Q3 Trading Update - RED

This is a big business, with almost $6bn revenues. It’s a global consulting & engineering group. The market cap’s just been smashed, from £862m last night, to only £509m at the time of writing, (09:30). It’s been a disaster for shareholders not just this year, but long-term too -

(By the way, I asked the boss at Stockopedia if I could use their graphics here, and he replied “Of course!”, so I’m grateful for that permission being granted).

My previous notes -

16/5/2024 - Shares 186p, announced mgt had rejected a 212p cash bid approach, saying it undervalued the business! (that is now 73p)

6/6/2024 - Shareholders pressurised mgt to let Sidara do due diligence re an increased 230p potential cash bid.

5/8/2024 - Shares plunge 38% to 132p, as Sidara calls off bid talks, blaming deteriorating macro. In line trading update. I reviewed the figures on Stockopedia, concluding AMBER/RED due to significant balance sheet concerns. Negative NTAV of $(677)m, including $307m liability for “asbestos related litigation” in the US, dating from the 1970s.

If that’s not enough to scare us off, I don’t know what is. Who would want to take on asbestos liabilities in the USA?!

On to today’s news.

“John Wood Group PLC ('Wood' or 'the Group') announces a trading update for the quarter ended 30 September 2024 ('Q3').”

The headline is not at all what I would associate with a 41% plunge in share price -

“Full year guidance confirmed”

Key points -

Annualised cost savings of $60m on track.

Two disposals - CEC Controls sold for $30m, EthosEnergy sale agreed $95m (plus possible $40m in 5 years from loan notes maturing) - might be delayed by regulatory approvals.

“Expanded margins” from higher pricing and focus on “sustainable solutions”.

Q3 trading “mixed”.

Projects business underperformed.

Q3 revenue $1,486m (+1%), and 9 month YTD revenues $4,330m (-3%).

Guidance -

"We have reiterated our full year guidance of high single digit growth in EBITDA and net debt to be broadly flat compared to last year, assuming the sale of EthosEnergy completes by year end."

“Group adjusted EBITDA for Q3 was lower than last year, with growth in Consulting and Operations more than offset by a decline in our Projects business.

Group adjusted EBITDA YTD was up 4% with very strong growth in Operations and modest growth in Consulting partly offset by the weakness in Projects. The group's adjusted EBITDA margin was up YTD, with higher margins across both Consulting and Operations.”

I’m struggling to see how any of the above justifies a share price crash of c.40%?

Ah, this next bit could be what has spooked the market - possible accounting problems flagged by the auditors -

“HY24 results and independent review

Following the exceptional contract write-offs relating to the exit from lump sum turnkey and large-scale EPC reported at the half year 2024 results1, and in conjunction with the auditor's ongoing work, the Board, in response to dialogue with its auditor, has agreed to commission an independent review to be performed by Deloitte.

This review will focus on reported positions on contracts in Projects, accounting, governance and controls, including whether any prior year restatement may be required. An update will be provided as appropriate following its conclusion.

The results presented in this trading update, and our full year outlook, are before any potential impacts from the independent review.”

This is very unusual, and naturally undermines the credibility of all the company’s numbers.

Order book is down -

“Our order book at 30 September 2024 was around $5.4 billion, down 8%2 compared to September 2023 and lower than the $6.1 billion position at June 20243. This reflects the phasing of large awards in our Operations business and ongoing weakness in Projects across minerals and life sciences, as well as delays in awards across chemicals.”

Outlook - bear in mind they just said that the EthosEnergy sales might not complete by year end! -

“While mindful of the weakness in our Projects business, we remain confident in the continued improvement in the cash trajectory of the Group, with improving operating cash flow and reducing exceptional drags. Our intention is to provide free cash flow guidance for FY25 at our full year results.”

Broker notes - nothing available on Research Tree. I tend to find that when a mid cap drops by c.40%, even if the RNS doesn’t sound too bad, it usually means some premium brokers have slashed forecasts by a lot (having spoken to the company and got privileged information & hints, no doubt), informed their paying customers, whilst we little people are kept in the dark.

Paul’s opinion - this is impossible for me to assess, due to inadequate information. A bit of softness in one division doesn’t sound too bad, and it reaffirms 2024 guidance. I can’t see any proper guidance for 2025 though, so perhaps brokers have quietly slashed 2025 forecasts this morning? That’s my best guess.

Plus it’s got all the existing problems I’ve mentioned before, of a horrible, overly indebted balance sheet, and the asbestos liabilities. We can now add an accounting review to those problems, which is only going to make the balance sheet worse. I can’t recall accounting reviews ever coming to a positive conclusion!

I’m glad I previously flagged the high risk here at AMBER/RED. Should I go to RED today? I think it has to be, since personally I never invest in any companies where accounting problems are discovered - have been stung too many times in the past. Sometimes it works out OK, but other times the problems are far worse than originally stated - look at Conviviality, and Patisserie Valerie, which turned into complete disasters (shareholders wiped out at both) after discrepancies were found.

I just can’t see the point in getting involved at Wood. So it has to be RED.

Maybe management should call Sidara, and ask if they want to buy it for less?

Live TOMORROW at 3pm (8th Nov) on https://x.com/VOXmarkets 'Smallcap Investing', I will be interviewing top notch stock picker & commentator Paul Scott as part of new weekly series (ie same time, same place every Friday at 3pm).

These flagship programs are sure to be fascinating, including our BEST SMALLCAP IDEAS OF THE WEEK.

Elsewhere, we'll also try to explain the broader macro outlook, key investment themes/principles, the significance of any market moving events (eg Trump election & BoE/FED interest rate decisions), and of course answer any of your questions.

Lastly, if anyone or any company would like to sponsor the Show (re naming rights), then please feel free to contact me here or via my email address paulhill@pmhcapital.com. https://x.com/VOXmarkets .

Everyone is welcome.

https://www.youtube.com/watch?v=fx6puuq21SE

The comments seem to have an improved layout now too, after I upgraded to "Publisher" today on Substack. Are you finding this layout better now? Thanks for bearing with me, this is all new to me too!!