Thu 3 July 2025 - Paul Scott's Small/Mid Cap Value Report

Starters: 3IN, FRAS, BCG, GPE, PEEL, PEN, Mains: STB, WOSG, QTX, CURY, AOM, IGP

Good morning from Paul, Dave, Jon, and Alun!

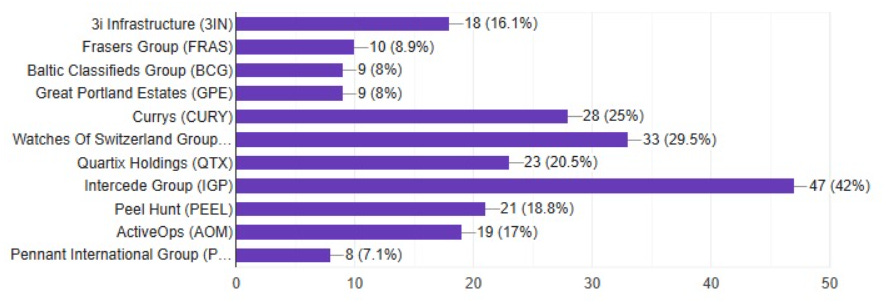

Reader Vote

Drum roll please …. here are the results -

We should have at least the top 4 done by lunchtime. EDIT - good, all done.

“Profitable Growth”

As regulars know, I detest the vague, ambiguous phrase “profitable growth”, because it’s designed to mislead. It’s not actually saying that profits will grow, but tries to sound like it is saying that. Hence it chips away at my confidence in a company, if I see this largely meaningless, and deceptive phrase in their RNSs.

So a special, positive mention goes today to Pennant International, which used this much better phrase -

“Pennant is strategically focused on sustainable recurring and repeatable revenues and profitability growth…”

PROFITABILITY GROWTH - is vastly superior, as this is directly saying that it expects profit to grow. Well done Pennant, and let’s hope more companies will push back on the ghastly “profitable growth”, and replace it with the far more precise and meaningful “profitability growth”.

We do notice these things, and it affects investor perceptions.

Firstly an apology, the incompetent Editor here (me!) overlooked a section that Dave wrote yesterday, on Secure Trust Bank (STB). What a remarkable share price recovery this special situation has delivered, well done to holders here.

Secure Trust Bank (STB)

Up 6% to 850p (£162m) - Strategic Pivot - Dave - NO COLOUR - DAVE HOLDS

What does it do?

Specialist lender.

Previous coverage:

Key points:

STB has announced that it will stop new lending within its Vehicle Finance business and put the existing book into run off. The decision reflects historical performance and the medium-term outlook for this part of the business.

Going forward, STB plans to

“increase capital allocation to its Retail Finance, Real Estate Finance and Commercial Finance businesses, which all have a strong track record of generating attractive returns”.

Vehicle Finance generated a loss (before exceptional items) of £21.8m in FY 12/2024 and accounted for nearly 30% of the group’s operating costs.

It is reiterated that:

“subject to no adverse changes in the economy and trading environment, the Group was well positioned in the near term to achieve its £4 billion net lending target, at which point it is expected to be at a scale to deliver a ROAE of 14-16%”.

STB has traded in line with management expectations in H1 (6m to 6/2025).

Balance sheet:

NTAV was £355m at 31 Dec 2024. STB currently trades at less than half this.

STB has some exposure to the FCA’s ongoing review into historical discretionary commission arrangements ('DCAs') in the motor finance market and the associated court cases.

A provision of £6.9m has currently been made in relation to this. However, there is still considerable uncertainty around the outcome and the eventual provision “could be materially higher or lower”.

Valuation/Pricing:

Adjusted PBT before impairments in FY 12/2024 was £100.9m (c.0.6x the current market cap).

Dave’s opinion:

Given the exposure to historical vehicle finance, STB is a special situation with a highly uncertain outcome. Even after recent share price gains, the market appears to be pricing in significantly more exposure than management currently expects.

A Supreme Court ruling is expected in July and that should give further clarity. The FCA themselves favour a redress scheme and update on this within six weeks of the Supreme Court’s decision. Given the uncertainty, STB has to remain NO COLOUR.

Click here for my special signup deal for new accounts at ShareScope. It’s terrific software, and helps fund our writers here from commissions earned.

End of free section. Tomorrow is Free Friday, so the whole report and podcast will be free then.

Keep reading with a 7-day free trial

Subscribe to Small/Mid Caps with Paul Scott to keep reading this post and get 7 days of free access to the full post archives.