Wed 27 Nov 2024 - Paul Scott's Small/Mid Cap Value Report

Free section: ATG, KETL, TRT Premium: PETS, AML, TUNE

MrC's Smallcap Sweep: KETL clicking on and off.

KETL, DGI, OMIP, IUG, TRT, ATG, MOTR, IOM, GTLY, TUNE

◄Strix (KETL)► leaves holders steaming as it warns FY-Dec adj pretax only £18-19m (at const FX). Blames continued weak sales. "The improvement in sales trends experienced in the Kettle Controls markets in the first six months of the year was due to a pipeline refill." The significant progress on the balance sheet in H1 gives resilience. Still plans to restart divs. [SP=60.2 Cap=144m]

◄DG Innovate (DGI)► signs JV deal with India's with EVage Automotive to to manufacture a range of DG Innovate's Pareta e-drives. This follows March's MoU. CEO trumpets "I haven't been this excited about a product launch since my days at Tesla...This is a momentous day for DGI". [SP=0.1 Cap=12m]

◄One Media iP (OMIP)► gets shot of TCAT to Round,a tech-enabled digital agency, for 5% of latter. Also makes £175k loan to Round. TCAT op loss in FY23 was £566k. [SP=3.79 Cap=8m]

◄Intelligent Ultrasound (IUG)► will state amount of planned capital return in Dec. Trading: year to 22 Nov rev £8.1m (down 12%) of which £0.7m is from discontinued ops. [SP=11.8 Cap=40m]

◄Transense Technologies (TRT)► AGM stmt - guides FY results at least in line with market expectation. First 4 months rev up 48% but net profit up only 10% due to "reflecting the costs added in preparation for scale-up of both Translogik and SAWsense". [SP=182 Cap=29m]

◄Auction Technology (ATG)► FY-Sep. Current trading in first 8 weeks: rev up 4-6% and EBITDA margin 45-46% "reflecting operational leverage from revenue growth offset by ongoing investment into the business". Co confident in ability to sustain this growth. [SP=440.5 Cap=543m]

◄Motorpoint (MOTR)► H1-Sep.returns to profit despite 7% rev fall. Retail volumes up 17%. Outlook - Strong momentum has continued into H2. No material impact on trading to date, post reintroduction of commissions. [SP=115.68 Cap=101m]

◄Iomart (IOM)► H1-Sep. Outlook sounds in line. [SP=94 Cap=104m]

In line: GTLY, TUNE

Good morning from Paul!

First off, apologies for yesterday’s report being late, and only covering 2 companies in depth (Severfield and Halfords). I’m full of cold unfortunately (everyone in London seems to be sick), although thankfully tested negative for covid last night. If yesterday was a 10-20% efficiency day, today feels like it’s going to be maybe 50-60%. I appreciate this is not ideal, but that’s where we are.

On the positive side, Mr Seamus took full advantage of the situation. He’s figured out that if he goes beserk when people get home from work in my London household, and I’m in bed, then the others assume I’ve forgotten to feed him. So he was fed dinner twice last night, not for the first time!

Here he is after a particularly severe grade 1 at the groomers last week - still going strong at 18 years old!

Still a few minutes to go until the 7am RNS fires up, so as usual I’ll draw up my to do list below.

Weds 27 Nov 2024 - SCVR agenda (free section)

Auction Tech (ATG) - Up 11% to 490p (£596m) - Final Results - AMBER

Flat EPS, but a marked reduction in net debt means my previous balance sheet concerns are now being resolved. It’s a good, cash generative business. However, profit is definitely ex-growth now, especially after broker forecasts are cut today by 8-10%. Not a good look when it accompanies a positive-sounding RNS.

Strix (KETL) - down 7% to 56p (£128m) - Trading Update - BLACK (profit warning). RED on fundamentals.

Warns on FY 12/2024 profit, with Zeus slashing forecast by 26%. I dislike the numbers here, in particular all the adjustments, and a horrible balance sheet with far too much debt. It’s never smelled right to me, and I remain negative, more so after this profit warning. Likely to continue falling I reckon.

Transense Tech (TRT) - up 6% to 190p (£29m) - AGM TU - AMBER/RED

At least in line trading update sounds good, but on closer inspection all the profit and most revenues are coming from a legacy contract that is peaking in 2025. Other activities have barely got off the ground financially. So I think the bull run in this share looks to be built on shaky ground.

Transense Tech (TRT)

Up 6% to 190p (£29m) - AGM TU - AMBER/RED

This one has been listed since 1999, round about the beginning of my investing career, so I’ve looked at it many times over the years. It was a blue sky thing, with supposedly revolutionary tyre pressure monitoring, that everyone got excited about in the original tech boom that blew up in 2000. Since then, it managed to commercialise one deal, which is generating cashflow, but the problem is that the clock is ticking on expiry of that deal, which the company calls a “residual royalty” which ends in 2030. So valuing TRT on current profits would obviously be a mistake, as they’re not sustainable.

For that reason I’ve tended to be sceptical, but the share price has been doing very well, so maybe a new generation of investors who’ve not heard the story before are getting involved?

“Transense Technologies plc, the provider of specialist sensing solutions and measurement systems, announces the following trading update for the first four months of the financial year ending 30 June 2025”

Today’s update sounds upbeat, concluding -

“Taking all of these factors into account, the Directors believe that the Company is well placed to achieve results at least in line with market expectation for the current year, and are optimistic of prospects thereafter.”

Broker research - a note from Allenby dated 23/9/2024 shows FY 6/2025 as £5.5m revenues, and £1.6m adj PBT. However it also says 2025 will be the peak year for iTrack royalties, reducing 40% thereafter. That’s a serious problem, because as you can see from the company’s slide below, the legacy iTrack royalties are by far the largest earner, and are 100% gross margin. This makes up more than the entire group profit, and is about to drop considerably, before expiring altogether in 2030. The other revenue streams are quite trivial, and are not growing much -

Paul’s opinion - I’ve seen enough to confirm my view that this share is best avoided. All the profit is coming from a short-life legacy contract. The other activities have barely got off the ground. Therefore I think the £29m market cap looks an accident waiting to happen, once the penny drops that this is a 25-year old project that is generating miniscule revenues, and has only survived from lucrative royalties from a single legacy contract.

It’s an avoid for me. I’d happily change to a more positive view, if it’s able to show exponential growth from new income streams, but there’s no sign of that as yet. Strip out the legacy royalties, and you’ve got a tiny, cash burning jam tomorrow project. That type of share hardly ever works, and it’s usually the biggest drain on our small cap portfolios.

Although this share certainly has momentum behind it… for now -

Strix (KETL)

Down 7% to 56p (£128m) - Trading Update - BLACK (profit warning). RED on fundamentals.

Revisiting its Oct 2023 all time lows again today. I don’t like this share, and last time I looked in June 2024 I concluded RED, due to excessive debt. Also its accounts have always looked odd to me, with poor cashflow and weird acquisitions. The whole thing has just never felt right, and it has a China connection too, which is a red flag in small caps.

What’s the latest?

“Strix Group Plc (AIM: KETL), the global provider of innovative sustainable water technologies, controls and complementary small domestic appliances, provides an update on trading for the financial year ending 31 December 2024 ("FY24").”

It’s quite a rambling account of what’s happening in the various group companies. Overall we’re told -

“As a result of the above, Strix now expects to report adjusted profit before tax for FY24 in the range of £18m to £19m (on a constant currency basis).”

What was the previous guidance? It doesn’t say.

Zeus clarifies, by reducing its FY 12/2024 adj PBT estimate from £23.6m to £17.5m, a decline of 25.7%. So I’d say the 7% drop in share price today has got off lightly, it should be considerably lower I think.

Looking back at the H1 results, there were large adjustments, and at a statutory level it was loss-making.

Net debt -

“Strix's debt position has remained a priority for the management team, with latest reported net debt leverage at c. 2x. Reflecting management's confidence in the underlying business, it remains the intention to reinstate the FY24 final dividend for payment in 2025.”

I’m not sure paying divis again is a good idea, or likely. The H1 results commentary previously said it is targeting debt reduction to 1.5x.

Paul’s opinion - I’m not comfortable with the accounts. There are lots of red flags, with large adjustments, a horrible balance sheet with negative NTAV and far too much debt still. Why get involved? We’ve got something like 1,300 UK shares to choose from, so if something doesn’t feel right to me, then I’m more than happy just to ignore it. RED again. That’s worked well so far.

Auction Tech (ATG)

Up 11% to 490p (£596m) - Final Results - AMBER

I’ve been quite sceptical about this auction services group, worrying that it looked largely ex-growth, and disliking its highly indebted, weak balance sheet. It was a 2021 float too, which like most of them, has been a poor investment to date. 2021 was very much the year when greedy brokers killed the IPO goose with overpriced & opportunistic floats that have nearly all gone wrong. Who would bother looking at any IPOs now, given the performance of the 2021 crop?

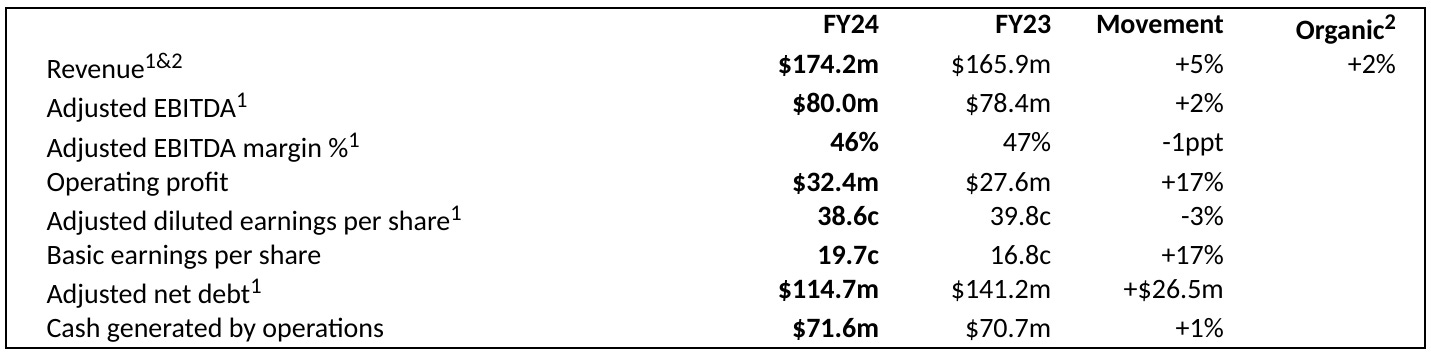

Highlights table - note the gulf between adj EBITDA and operating profit. Also, it omits my preferred measure of adj PBT, probably because that hides the hefty net finance costs line of $14.0m, which takes operating profit of $32.4m down to PBT of $18.4m. That’s only 23% of adj EBITDA remaining by the time we get down to PBT! -

The reconciliation between PBT and EBITDA is quite helpful. Note that the largest item is effectively goodwill amortisation (mangled up by accounting standards to show totally made up figures for brand, customer relationships, etc, which is all complete nonsense in my view). I would be happy to add back the $32.5m amortisation charge, to get to adj PBT by my calculations of around $51m. So it’s a proper business, with genuine profit I think -

Tax - note the P&L shows negative tax charges, which boosts PAT. However, I’m pleased to say that in note 3 this seems to be adjusted out, hence the $47.8m PAT looks reliable (down 2% on LY), giving adj diluted EPS of 38.6c. Convert into sterling at $1.25, and it’s 30.9p EPS. At 441p/share the PER is 14.3x - that looks about right to me for a mature business with a fair bit of debt still.

I’ve just noticed shares are up 10% in early trades, so let’s rework the PER based on 482p/shares, it’s now 15.6x.

Balance sheet - is full of nonsense, so let’s get rid of all the intangible assets and the (usually related) deferred tax. That means a net $800m to come off the NAV of $688m. Leaving a negative NTAV of $(112)m, far from ideal.

However, like most software companies, it has almost nothing in physical fixed assets, and no inventories. Therefore it can operate fine with a weak balance sheet.

Also I’m really impressed with the debt reduction, which over the last 3 years has gone $167m, $133m, and most recently $99m. Those numbers are the gross long-term debt. I think this demonstrates that it’s doing an impressive job in paying off previously excessive debt, and hence I’m now much more comfortable with this balance sheet. We just have to hope they don’t go on another acquisitions spree and send the debt back up again. It’s expensive borrowing money these days, as you can see from the hefty finance charges.

Overall though, my balance sheet concerns are now largely resolved.

Cashflow statement - is good, for both years. This is a genuinely cash generative business. It uses about one-sixth of cashflow for capitalised development spending, which is not excessive. As mentioned above, the rapid debt reduction is evidence that this is a good, cash generative business. I’m warming to this share!

Outlook - nothing madly exciting here, and again it’s the very modest revenue growth that underwhelms, and means I’m inclined to value it as a mature business, not an exciting growth company -

Broker update - this is a bit surprising. Cavendish has reduced forecasts today, lowering FY 9/2025 by 8% from 43.2c to 39.6c. It also lowers FY 9/2026 by 11% to 43.6c. This is really not a good look - an RNS which sounds upbeat, but then significant cuts are made to broker estimates, I hate that kind of thing, and it completely undermines my slowly building enthusiasm for this share. This is effectively a profit warning today, but slipped out via the broker, not explicitly in the RNS.

Paul’s opinion - it was starting to look interesting, but for me the significant cuts to broker forecast earnings today completely undermines the bull case. I wonder if people buying the shares this morning at a 10% higher price were aware that forecasts had just been cut?

I’d say it looks priced about right, for a mature, ex-growth business. The balance sheet looks much better now, or less bad anyway. I see it rules out paying dividends in the foreseeable future, which I think investors should push back against. It’s a good discipline for cash generative businesses to pay their owners divis. I suspect ATG probably wants to create the illusion of growth by making more acquisitions. There isn’t any organic profit growth in evidence, in the numbers or the forecasts.

Note also that the original private equity owner did a secondary placing at a discount in July 2024. I wonder if they’ll be looking to offload more?

The competitive situation would need careful scrutiny. I remember when we have previously discussed ATG on Stockopedia, some readers flagged client dissatisfaction with its high charges, and I believe there was a competitor undercutting it? If you have any sector knowledge please do leave a comment.

Overall, AMBER looks about right to me.

I didn’t intend to look in this amount of detail, but Paul Hill mentioned this stock (which he likes) in our Friday catchup last week, so it was front of my mind today.

Share possibly finding a floor maybe?

Keep reading with a 7-day free trial

Subscribe to Small/Mid Caps with Paul Scott to keep reading this post and get 7 days of free access to the full post archives.