Fri 8/11/2024 - Paul Scott's Small Cap Value Report - RMV, EMR, SRP, INDV, VTY, WIZZ, IAG, BOO, CYAN

This article is now complete.

Good morning from Paul!

Daily podcast -

3pm today - I hope you can join me & Paul Hill, on Vox Markets, for our new live weekly market roundup! If enough people like it, we’ll do these every Friday. I think there will be a recording too, to watch later. UPDATE: here’s the recording of it -

Timestamps -

00:00 Paul’s new SCVR service on Substack

02:15 Impact of the Budget

08:00 Fallout from the US Presidential election

10:40 Hunting (PS holds)

15:50 Vistry

21:30 Michelmersh Brick (PH Holds)

25:50 OneSavingsBank

33:15 Kooth (PS holds)

37:50 Gooch & Housego (PH holds)

44:00 Smiths News

49:10 Plexus (PS holds)

53:45 Equals (PH holds & Vox client)

55:45 Venture Life (Vox client)

61:15 Anpario

64:10 Time Finance

Let me know what you think in the comments below. Should me & Paul Hill continue with this weekly recap? Does it add value for you?

Right, I’ve got the IT fixed I think! Quite a few people have said they struggle with Substack and find it difficult to navigate. So I’ve changed the format, which is now much better, and just looks like a normal website. Please bookmark this link in your web browser, and use this to visit my articles more easily in future.

Or, if you are an existing user of the substack app, then carry on accessing my stuff through that.

Reader comments - I’ve tinkered with the settings, and these are now much improved, and are just below each article, with the newest comments at the top, so very similar to Stockopedia now, you should find it’s easy to use from now on. The functionality is fairly limited, but there we go.

Chat - I enabled this facility yesterday, to try it out, but I think it’s going to be no good, as it just duplicates comments, and it would take up far too much time for me to monitor it all day, and distract me. So unless people have a strong objection (let me know in the reader comments if so) then I’ll switch off chat shortly.

Subscription pledges from you are pouring in, I’m absolutely thrilled at how many readers have pledged to subscribe at my very reasonable £10/month or £100/year fee. Think how much content I produce in a year! That will be about 250 daily reports + podcasts. And occasional CEO interviews, plus of course my Top 20 shares ideas for 2025 (both 2023 and 2024 out-performed AIM by 20-30%), and access to my quick reference spreadsheet. Subscriptions will be turned on in 1-2 weeks.

I want it to be good value, so that we attract a good community here posting comments which add value. Also once we get beyond an achievable target subscriber number, I’ll have enough income to employ a second writer to join me. In the meantime though it’s a one man band, so there isn’t any backup sickness cover for the moment.

Whilst this substack is free, I need to attract as many readers as possible, so anything you can do to help (retweeting links to finished articles, etc) would be incredibly helpful. So far so good, and thanks again to everyone for all your lovely messages, subscription pledges, and spreading the word to your friends - hugely appreciated! I feel greatly encouraged that this project is quickly becoming a success, and we’ve only just begun!

Summaries

Vistry (VTY) - down 20% to 700p at 10:16 (£2.33bn) - Trading Update (profit warning) - BLACK / AMBER/GREEN on fundamentals.

Main section below is on the profit warning from Vistry, where I see a potentially interesting buying opportunity possibly beginning to emerge, but it’s anyone’s guess where the bottom will be.

Brief Comments

Looks like the Employer NICs costs is sinking in with investors - I see the top fallers list includes big employers, eg Greggs (down 6% today), Halfords (down 5%), Tasty (down 5% - nanocap restaurant chain). It looks too early to me to bottom fish, although it was interesting to see Wetherspoons has come off its recent lows. I’m watching from the sidelines for now, but it might soon be time to do some tentative toe dipping, who knows? After all, the higher costs don’t kick in until April 2025, which gives big employers time to plan price rises, and other mitigating actions.

Boohoo (BOO) - publishes a robust response to the attacks from Mike Ashley’s Frasers Group (FRAS). Key points -

BOO thinks its shares are undervalued.

Continuing strategic review, which will take “several months”.

BOO works in interests of all shareholders, pointedly “not just Frasers’ self-interest”

FRAS can only have a NED on BOO’s board, subject to governance controls (refused so far by FRAS).

Calls FRAS’s open letter “inaccurate and misleading” as ignored BOO’s offer of a meeting.

FRAS is not an independent shareholder, it is a competitor.

”Wholly inappropriate” for FRAS to use its BOO shareholding to promote its own self-interest.

Founding Kamani family own 23.2%, and do not intend bidding for BOO - so interests are aligned with other shareholders (apart from FRAS, presumably!)

”Continual legal letters and public posturing” by FRAS “not conducive to maximising value for all shareholders”.

Paul’s view - I might be able to mediate here. My suggestion is sort it out through either handbags at dawn, or a drunken dance-off between Big Mike and Mahmud! They both enjoy a skinful.

CyanConnode (CYAN) - down 8% to 10.7p (£38m) - H1 Results - RED

More poor results from this jam tomorrow serial disappointer. It’s trying to sell smart meters in India, and always talks up the pipeline & order book, but it always posts losses - H1 was little changed on last year, £5.6m revenues and c.£2m loss. Promises a Q4 weighting to trading, as happened last year, but it still made a loss even when H2 revenue doubled last year. It looks hopeless to me.

Customers don’t like paying its invoices, with receivables once again greater than H1’s entire revenues. Raised £5.4m cash in a placing just before the H1 period end, but only £3.7m remained at end Sept 2024 after paying stretched creditors. NTAV is £10m, but that’s entirely made up of receivables which I think could be bogus. Tries to finesse away a “material uncertainty” going concern warning.

Paul’s opinion - very negative, I think this could end up at zero. The numbers are a Victor Meldrew for me, and I wouldn’t even bother looking at forecasts, given the track record. Happy to be proven wrong, but why take the risk of getting involved here?

Airlines - I see Wizz Air (WIZZ) is up 7% today to 1,475p, on a positive reaction to yesterday’s interim results, and read-across from IAG today perhaps. Remember that WIZZ has a weak balance sheet, making it by far the riskiest of the budget airlines. Whereas Easyjet, Jet2 and Ryanair all have strong balance sheets. Something to bear in mind before you start comparing PERs.

International Consolidated Airlines (IAG) is up today, +6%, on Q3 results.

Indivior (INDV) - down 2% to 778p (£981m) - Oaktree letter - NO COLOUR

Oaktree Capital (Howard Marks US giant fund manager) is sniffing around Indivior. Press reports say that Oaktree (7.4% holder) published an open letter, urging INDV to refresh its board and strategy, to improve performance. I’ve searched but can’t find this letter, so please leave a link in the comments if you have it. INDV responds today, saying it is “open minded about all proposals to enhance value creation”, sounds intriguing. I’ve flagged this share as potentially interesting several times earlier this year. The forward PER is very low, but there are some complications eg litigation problems. See Stockopedia on 25/10/2024 for my review of the Q3 results. No colour from me, as it’s too specialised. Press speculation over the potential for a takeover bid.

Frontier Developments (FDEV) - mentioned yesterday, dropping c.20% on rumours of a new games release having flopped. It’s down another 10% today to 214p. Checking back, on 13/9/2024 I mentioned being tempted to have a punt, based on improving results and a positive outlook comment. Plus the cash position looked OK at £29.5m (at 31/5/2024). Given the big drop in share price this week, the company must issue a market statement pronto.

Wood Group (WG.) - I see it’s bounced 11% to 55.5p so far today, after yesterday’s calamitous c.60% crash. I’m trying to resist the temptation to trade the bounce here, as I don’t normally do very well on that kind of thing. That £30k loss on Conviviality left a deep scar - sometimes you have to lose money to learn lessons that you don’t forget! Wood may be firming up today (no sniggering from my US readers please!), but they basically told us yesterday that we can’t believe any of their previous numbers.

Serco (SRP) - down 11% to 158p in early trades £1.64bn - Lost Contract & NICs - BLACK (profit warning)

Has lost long-running contract for Australian immigration detention services. Impact: £18m future profit lost (6% of forecast total profit). Expect a similar drop in share price today, maybe more, we’ll soon find out!? Also -

“UK national insurance

Tax changes announced by the UK Government in the budget on 30 October will impact our business. We estimate the combination of lowering the earnings threshold at which employers start paying national insurance contributions from £9,100 to £5,000 and increasing the rate from 13.8% to 15.0% will increase our direct labour costs by around £20m per year. The changes will be effective from April 2025 and we are actively exploring ways to offset these costs.”

Does it have wage cost inflation clauses in its customer contracts, I wonder? Will a tax hike fall within those contract terms for wage costs, I wonder?

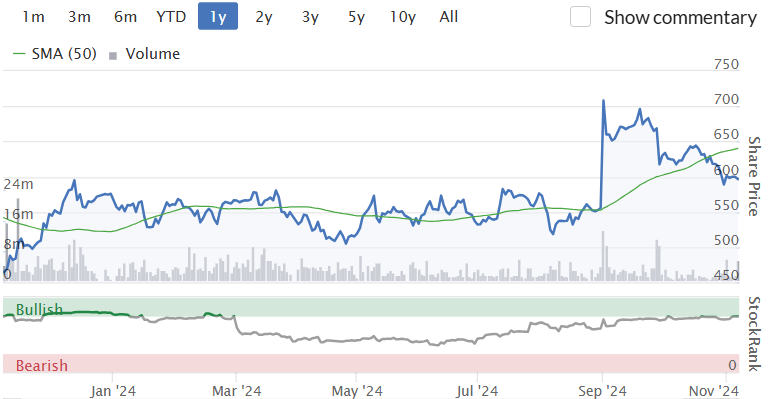

Rightmove (RMV) - 596p (y’day) £4.70bn - Q3 TU - AMBER/GREEN (moderately positive)

In line update for FY 12/2024 -

“We are in line to meet market expectations for revenue and adjusted underlying operating profit for the year…”

Dominant residential property portal in UK. “Greater optimism” among partners (estate agents) than this time last year. House prices growing slightly, and mortgage rates stable, and favourable outlook for more bank base rate cuts (Paul: I wouldn’t be so sure about that, with higher inflation likely from April 2025 due to budget impact, and mortgages are priced off gilts, where yields have gone up lately).

“Property transaction flow is improving”. Rental growth continues to moderate. New build activity still subdued, and less than last year.

Astonishing 70% operating profit margin, as expected. Sometimes accused of exploiting, price gouging from its near-monopoly position (“80% of customer time”).

Driving higher revenues per client, from product upgrades & upsells, “Optimiser Edge” premium package.

Paul’s view - a remarkable business, which generates colossal profit margins & cash. Peaked at 700p when Rupert Murdoch tried to buy it (780p mooted bid, part cash, part shares), but that was declined. Now down to 600p, and fwd PER of 20.7x looks justified to me. Divis poor at only 1.8% though, but it uses cashflow to do buybacks regularly, so share count is declining, enhancing EPS growth (copying NXT!)

I’ve previously been sceptical about the valuation, but at 600p I think this might be an attractive long-term entry point. You have to be sure that it can maintain its market dominance forever though. The Aussies were prepared to pay 780p for it, so at 600p in the market now, that looks a pretty good deal to me. So I’ll up my view to AMBER/GREEN.

Empresaria (EMR) - 28p (pre-market) £14m - Sale of tiny subsidiary - AMBER/RED

Announces it has sold Japanese subsidiary (breakeven in 2023) for nil, but got back £253k of a £455k intercompany loan (balance presumably written off, or deferred?) Simplifying group. Four smaller operations now exited.

Paul’s view - makes sense to simplify this random international mix of small staffing companies. EMR warned on profit recently, 22/10/2024, and needed a relaxation of bank covenants, so it’s higher risk (AMBER/RED last time). Personally I’m not interested, due to weak balance sheet.

My sector pick for a small, low quality staffing company is Gattaca (GATC) [I hold a small position] because the market cap is almost covered by net cash.

It might soon become a good time to look at buying some mid cap staffing companies for a cyclical recovery, although no sign of that as yet (internationally, not just UK). I’ve previously quite liked RWA and STEM, both have good balance sheets and quite attractive divis. Plus there should be a cyclical recovery to earnings at some point, when companies begin hiring again. Quite an interesting sector, possibly.

Bulls might say that if EMR can recover to previous profitability c.£5-10m pa, then this share could multibag from these lows. Who knows?

Main Section

Vistry (VTY)

Down 20% to 700p at 10:16 (£2.33bn) - Trading Update (profit warning) - BLACK / AMBER/GREEN on fundamentals

We had a nasty profit warning (down 28% to 908p) on 8/10/2024, when this contract housebuilder dropped a bombshell that its southern division had under-budgeted costs by a whopping £80m for FY 12/2024. A bounce to peak at c.1,000p only lasted 10 days, with declines resuming and today a 20% daily fall (at 10:16) to only 700p.

The latest news today is a further £25m hit from a full independent investigation to 12/2024 profit from the southern division’s inability to budget correctly, and additional £20m hit to 2025. Not a big surprise really, and not a huge amount. Good news - it reviewed the other 5 divisions, and found “no systemic issues” - does that wording give wriggle room for minor issues begin found, I wonder? Yes it does! -

“In addition, there have been a number of small value adjustments from the detailed CVR and other reviews carried out across the other 22 regions which in aggregate have resulted in a reduction to the Group's adjusted profit before tax in FY24 of £8m.”

Recent trading in Sept & Oct “slower than anticipated”, but average weekly sales YTD are up a healthy 42% on last year. Remember that Vistry operates through a partnership model, so this may not necessarily have read-across to the other housebuilders, who target mainly the private sales market. Reasons -

“The Partner Funded market has been quieter during September and October reflecting both a slowdown in partner activity ahead of the Autumn Budget and later than anticipated reductions in the borrowing rate, particularly impacting the timing of partner transactions requiring higher levels of funding.”

Good news here -

“We were pleased to see the Government's commitment to a social housing rent settlement for the next five years in the Autumn Budget and the additional £500m for the Affordable Homes Programme, increasing the annual budget to £3.1 billion.”…

“We continue to see strong demand from the private rented sector (PRS), particularly for portfolios of Single-Family Homes, with increased momentum from fund managers and PRS platforms looking for larger scale investment. Pricing on PRS units has remained competitive.”

Revised adj PBT guidance FY 12/2024 of £300m. Where’s the previous guidance figure? They’ve omitted it, so annoying when companies try to hide the comparison. I’ll have to waste time and look back now. Ah here it is, on 8/10/2024 it guided adj PBT of c.£350m. So today is a hefty £50m drop in profit guidance, half from the accounting mess up, and half from under-performance in recent trading.

Outlook - rather mixed below, with VTY echoing Persimmon recently mentioning that inflationary pressures are feeding through into 2025 -

“We have a strong forward sales position up 12% on prior year and totalling £4.8bn (2023: £4.3bn), supporting our FY25 delivery and beyond. The Group's growth in FY25 will be influenced by our need to stabilise the South Division and prevailing market conditions.

Having seen a year of neutral build cost inflation in FY24, the Group is expecting to see some overall pressure on build costs in FY25. We will look to mitigate these where possible through our benefits of scale and visibility of revenues, and through efficiency gains. We are assessing the impact of the Autumn Budget and note that the direct impact to the Group of the April 2025 increase in Employer National Insurance contributions will be c. £5m in FY25, with the rate increase also impacting our supply chain.”

Possible cuts/delays to dividends & buybacks maybe? -

“The Group remains confident in its Partnerships strategy and committed to its medium-term targets and capital distribution policy, with the timeframe of delivery under review.”

It remains committed to its medium-term targets including the distribution of £1bn of capital to its shareholders. In light of the recent issues in the South Division, the Group is reviewing the timeframe in which these are expected to be achieved.

Pauls opinion - there’s a lot to unpack here. The market doesn’t like it, with shares now down 20% today, to 700p (at 10:16). Amazingly, Vistry has now halved in share price in just 2 months. So is it a bargain? Actually, I’m going to be bold here, and say yes I think it might be getting into bargain territory.

The market cap at 700p is £2,328m. Whilst last reported balance sheet NTAV was close at £2,124m. So the price/tangible book is only 1.1x after today’s drop in share price. That is attractive I think.

Maybe best to ignore me though, as I got this completely wrong in the past, thinking that VTY was the pick of the bunch in the housebuilding sector, due to its differentiated partnership model.

My main worry was that the accounting problems in the southern division could be the tip of the iceberg. It now transpires that there are not similar problems in the other 5 divisions, which I find reassuring.

Overall then with it now halved in price, this share looks quite interesting to me, for investors with a strong stomach. The balance sheet now protects 90% of the new, lower share price, which should be getting close to a low point in the share (famous last words!). I think risk:reward therefore is starting to look interesting. AMBER/GREEN from me.

A few people have mentioned about including images and pictures in the comments section. This is not possible on substack it seems. However what you can do is make a note and then post a link to it:

https://substack.com/profile/139763592-benhazz/note/c-76142750

Enjoying the new Substack Paul - very well done